How APAC Health Systems Manage the Financial Cost of AI Adoption

APAC health systems manage AI costs through phased rollout, shared funding, and ROI-driven use cases

Executive Summary

- Health systems across the APAC Region face significant financial barriers to AI Adoption, particularly among small and mid-sized hospitals with constrained capital budgets.

- Cost management strategies increasingly emphasize long-term ROI planning, phased deployment, and prioritizing “low-risk, high-impact” use cases such as workflow automation and administrative AI.

- A clear divide exists between one-time CapEx investments and recurring OpEx costs.

- Governments and system leaders are using public funding, shared AI centers, cloud-based pricing models, and partnerships to reduce duplication and spread costs across networks.

- Governance, data readiness, and workforce upskilling are now recognized not as optional add-ons, but as core cost drivers that determine whether AI investments scale or stall.

Why Cost Is the Central AI Question in APAC Healthcare

Across the APAC Region, enthusiasm for artificial intelligence in healthcare is high—but budgets remain tight. Surveys and qualitative studies consistently show that while hospital leaders recognize AI’s potential to improve efficiency, quality, and access, financial cost is the single most cited barrier to adoption, especially outside top-tier academic and tertiary centers.

Unlike many Western systems, APAC health systems operate under heterogeneous funding models, ranging from highly centralized public systems (e.g., Singapore, Brunei) to fragmented, mixed public–private ecosystems (e.g., Indonesia, Vietnam, the Philippines). This diversity means there is no single economic model for AI Development. Instead, hospitals must navigate constrained capital, uneven digital maturity, regulatory uncertainty, and rising workforce costs—all while being pressured to demonstrate value.

This article examines how APAC health system stakeholders are managing the financial cost of AI adoption. The focus is not on hype, but on the economic mechanisms, trade-offs, and governance choices shaping real-world deployment.

AI Investments Set to Outpace Digital Tech Spending in Asia-Pacific, Driving $1.6 Trillion Economic Impact by 2027. Read more here!

Understanding the Cost Structure of AI in APAC Health Systems

A. One-Time vs. Recurring Costs

A recurring insight from HIMSS25 APAC and regional studies is that hospitals often underestimate recurring costs while over-focusing on initial pilots.

One-time (largely CapEx) costs include:

- Digital infrastructure upgrades (EHRs, data platforms)

- Initial AI software licenses or development costs

- Hardware or on-premise server investments (where required)

- Initial data cleaning and system integration

Recurring (largely OpEx) costs include:

- Cloud compute and storage (pay-as-you-go models)

- Model monitoring, validation, and retraining

- Cybersecurity and data privacy compliance

- Workforce training, reskilling, and change management

- Insurance and liability coverage (where applicable)

Dr. Gao Yujia of Singapore’s NUHS emphasized that non-tertiary and district hospitals inherently lack budget flexibility, making recurring OpEx commitments particularly challenging over multi-year horizons.

B. Pilot Economics vs. Scaled Deployment

Many APAC hospitals succeed in pilots—but stall at scale.

- Pilots are often grant-funded, vendor-supported, or subsidized.

- Scaling exposes hidden costs: integration across departments, interoperability with legacy systems, expanded cybersecurity budgets, and sustained workforce support.

This explains why panelists at HIMSS25 APAC stressed 3–5–10 year ROI roadmaps, rather than 12–18 month pilot evaluations. Without long-term financial modeling, AI projects risk being discontinued once pilot funding ends.

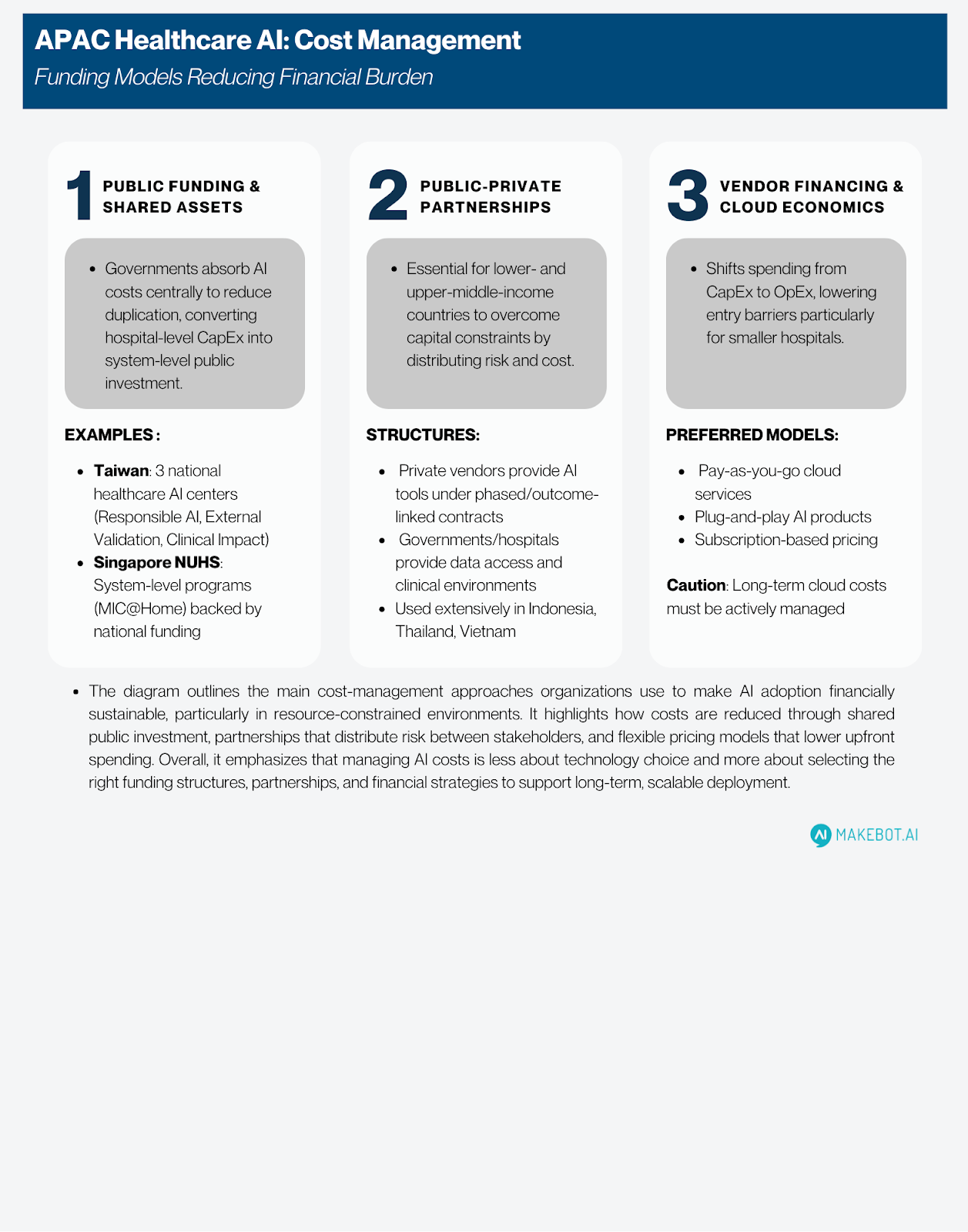

Funding Models Used to Reduce AI Financial Burden

A. Public Funding and Shared National Assets

Several APAC governments are absorbing AI-related costs centrally to reduce duplication:

- Taiwan has established three national healthcare AI centers (Responsible AI, External Validation, Clinical Impact Evaluation), allowing hospitals to share evaluation, validation, and governance costs.

- Singapore’s NUHS operates system-level programs (e.g., MIC@Home) backed by national funding, reducing per-hospital investment requirements.

These models convert what would be hospital-level CapEx into system-level public investment, improving affordability and standardization.

B. Public–Private Partnerships (PPPs)

In lower- and upper–middle-income countries, PPPs are essential to overcoming capital constraints:

- Private vendors provide AI tools under phased or outcome-linked contracts.

- Governments or hospital systems provide access to data, clinical environments, and scale.

- Risk and cost are distributed rather than borne entirely by hospitals.

Participants from Indonesia, Thailand, and Vietnam highlighted PPPs as one of the few viable paths to AI Development under limited public budgets.

C. Vendor Financing and Cloud Economics

Hospitals increasingly prefer:

- Pay-as-you-go cloud services

- Plug-and-play AI products

- Subscription-based pricing instead of large upfront licenses

This shifts spending from CapEx to OpEx, lowering entry barriers—particularly for smaller hospitals. However, cautions that long-term cloud costs must be actively managed to avoid cost creep.

Procurement, Reimbursement, and ROI Justification

A. Procurement Constraints

In several APAC countries, procurement rules themselves inflate costs:

- Administrative delays in acquiring servers or software (Vietnam, Indonesia)

- Unpredictable public-sector purchasing cycles

- Fragmented standards across hospitals

These inefficiencies increase total cost of ownership, even when AI tools themselves are affordable.

B. Reimbursement and Insurance Gaps

A major unresolved issue is who pays for AI-driven care:

- AI tools are rarely reimbursed as distinct clinical services.

- Errors and omissions insurance for AI remains unclear.

- Some clinicians fear AI could increase insurance premiums rather than reduce them.

Panelists compared healthcare to the automotive sector, where AI safety features lower insurance costs. In healthcare, the reverse is often true—an evidence gap that remains unresolved in current policy frameworks.

Build vs. Buy: Financial Trade-offs in AI Development

A. In-House Development

According to KPMG, 85% of healthcare organizations globally are building AI in-house, driven by:

- Desire for customization

- Data sovereignty concerns

- Long-term cost control

However, in APAC LMICs, in-house development is often financially unrealistic without foundational digital infrastructure and skilled talent.

B. Buying and Adapting External Solutions

Many APAC hospitals adopt a hybrid approach:

- Buy validated external tools

- Localize and validate them with local data

- Use shared validation centers to reduce cost

This approach aligns with concerns raised in Thailand and the Philippines about contextual accuracy and safety, which directly affect long-term cost and liability.

KPMG: AI's Extensive Adoption in Healthcare. Read here!

Governance, Risk, and Compliance as Cost Drivers

A. Technology and Data Governance

Governance is often perceived as a regulatory hurdle—but consistently show it is also a cost-control mechanism:

- Clear guidelines reduce rework and liability

- Standardized validation prevents unsafe deployments

- National data governance reduces duplication

Participants stressed that poor governance increases cost, not reduces it.

B. Cybersecurity and Data Protection Costs

Cybersecurity has become a non-negotiable AI expense:

- IDC reports that by 2026, 40% of APAC healthcare organizations will adopt AI-based threat intelligence.

- Ransomware incidents have forced hospitals into manual operations, with significant financial losses.

Security spending is now treated as part of AI OpEx, not a separate IT line item.

Workforce Upskilling and Operational Redesign

Workforce costs are among the most underestimated AI expenses:

- Training clinicians to trust and use AI

- Redesigning workflows to capture productivity gains

- Addressing resistance and job security concerns

BCG data shows APAC leads in GenAI usage—but governance and workflow redesign lag behind, creating inefficiencies that dilute ROI. Hospitals that fail to redesign workflows often pay for AI without realizing savings.

Practical Recommendations for APAC Health Leaders

- Model AI ROI over 3–10 years, not pilot cycles

- Separate CapEx and OpEx early in budgeting

- Prioritize workflow and administrative AI first

- Use shared services and national platforms where possible

- Favor phased, outcome-linked vendor contracts

- Invest in governance early to avoid downstream costs

- Treat cybersecurity as core AI spending

- Redesign workflows alongside deployment

- Build workforce literacy before scaling AI

- Align AI use cases with national health priorities

Showcasing Korea’s AI Innovation: Makebot’s HybridRAG Framework Presented at SIGIR 2025 in Italy. More here!

Conclusion

Across the APAC Region, the challenge of AI adoption is not technological ambition—it is financial sustainability. Health systems that succeed are not those spending the most, but those allocating costs strategically, aligning funding models with long-term value, and embedding governance into financial planning.

The evidence shows that AI can improve efficiency, access, and care quality—but only when hospitals move beyond pilots, invest in foundations, and manage AI as a system-level transformation, not a standalone tool. As Generative AI and advanced automation scale, cost management will increasingly determine whether AI deepens inequities—or becomes a shared asset across APAC health systems.

The financial question is no longer whether AI is worth investing in, but how APAC health systems design models that make AI affordable, accountable, and sustainable at scale.

Makebot: Turning AI Strategy into Scalable, Cost-Efficient Execution

As APAC health system leaders move beyond pilots, the real challenge is scaling AI Adoption without escalating costs or operational risk. Makebot bridges this gap by delivering industry-specific LLM agents and end-to-end Generative AI solutions designed for healthcare environments—helping organizations achieve faster ROI while keeping long-term CapEx and OpEx under control.

With ready-to-deploy solutions like BotGrade, MagicTalk, MagicSearch, and MagicVoice—powered by HybridRAG, presented at SIGIR 2025—Makebot enables rapid PoC-to-production with up to 90% cost reduction and a 26.6% accuracy improvement. From strategy to execution, Makebot helps APAC healthcare leaders turn AI Development into measurable, sustainable impact.

👉 www.makebot.ai | 📩 b2b@makebot.ai

.jpg)

.png)

_2.png)