APAC AI Outlook 2026 Signals AI's Breakout Moment as a New Revenue Driver

APAC AI has crossed from cost tool to revenue engine, with 96% of enterprises increasing investment.

Introduction

For years, artificial intelligence in the Asia-Pacific region was treated as a sophisticated experiment — a promising but peripheral investment justified primarily by cost reduction and process efficiency. That era is ending. The APAC AI Outlook 2026, anchored by research from IBM, IDC, S&P Global, and leading enterprise intelligence firms, reveals something more structurally significant: enterprise AI adoption across the region has crossed a decisive threshold, and AI is completing its transition from an operational tool into a direct engine of revenue growth.

This shift is not incremental. Across banking, telecommunications, manufacturing, healthcare, and retail, APAC enterprises are deploying Generative AI, Large Language Models (LLMs), and sophisticated AI Chatbot platforms not merely to automate tasks, but to create entirely new business models, unlock differentiated customer experiences, and generate measurable top-line impact. The investment numbers, the executive priorities, and the early commercial results all point to the same conclusion — 2026 is the year AI moves from the pilot stage to the profit stage across Asia-Pacific.

This article analyzes the strategic forces driving that shift, examines where the most significant AI revenue growth opportunities are emerging, and outlines what enterprise leaders must understand to compete in an AI-defined APAC market.

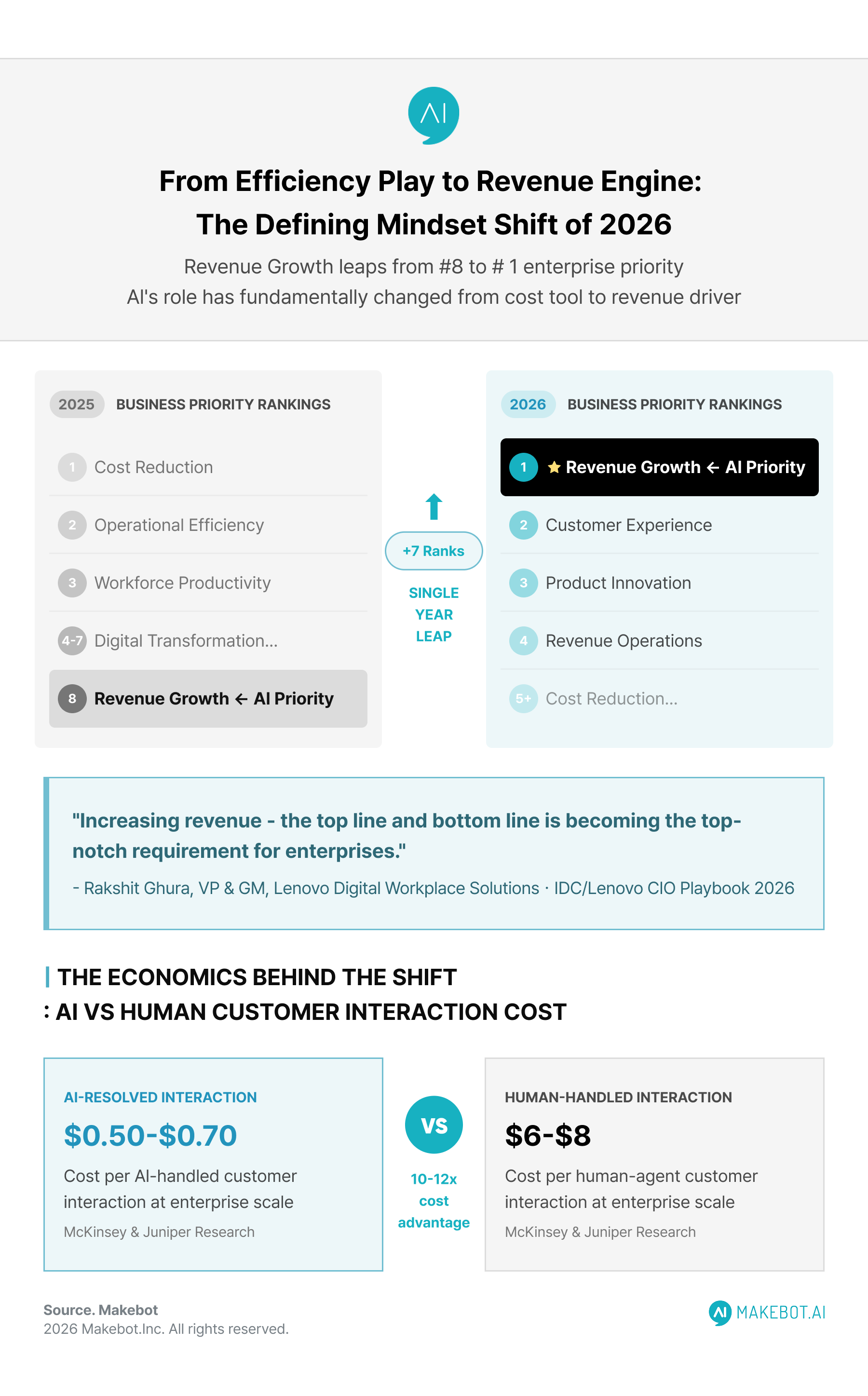

From Efficiency Play to Revenue Engine: The Defining Mindset Shift of 2026

The clearest signal of 2026's significance is not found in a technology benchmark — it is found in a change of executive priorities. According to the Lenovo CIO Playbook 2026, conducted in partnership with IDC, revenue growth has leaped to the top business priority for APAC enterprises, having ranked eighth just one year prior. This is a structural re-evaluation of what AI is for.

Rakshit Ghura, Vice President and General Manager at Lenovo's Digital Workplace Solutions, articulated this precisely: "Increasing revenue — the top line and bottom line — is becoming the top-notch requirement for enterprises." This represents a decisive departure from the prior generation of AI investment, which was largely justified through headcount reduction or workflow compression.

IBM's Institute for Business Value, in its landmark APAC AI Outlook 2026: Transferable Value across Industries report — developed through in-depth conversations with leaders from 14 top-performing organizations across banking, manufacturing, telecom, energy, and public services — found that:

- 64% of organizations are now redirecting AI investments toward core business functions with direct customer and revenue impact.

- 95% of global executives expect Generative AI initiatives to become at least partially self-funded by 2026, reflecting a widening commercial return on AI deployment.

- The most advanced APAC enterprises are no longer measuring AI against cost savings — they are measuring it against new revenue streams, new product categories, and differentiated market positioning.

What makes this shift durable rather than cyclical is the underlying infrastructure maturation across APAC. Cloud-native AI-as-a-service platforms, vertical foundation models, and expanded GPU and edge computing capacity have dramatically lowered the barriers to production-grade AI deployment, particularly for mid-market enterprises that previously lacked the technical resources to compete at scale.

How APAC Health Systems Manage the Financial Cost of AI Adoption. Read more here!

The APAC AI Market in Numbers: Scale, Speed, and Strategic Weight

The APAC AI market is growing at a pace that demands serious strategic attention from any enterprise operating in the region. Key market indicators as of 2026 include:

- The APAC AI market is projected to reach US$295.30 billion by 2030, expanding at a compound annual growth rate of 28.58% from 2024 to 2030. (Statista)

- The Asia-Pacific Generative AI market is on course to reach $53.96 billion by 2033, up from $3.06 billion in 2023 — a 33.24% CAGR over the decade. (BIS Research)

- APAC is now the fastest-growing region globally for Generative AI business revenue, with projected 65% year-over-year growth in 2026 alone. (451 Research / S&P Global)

- The Enterprise AI market stands at $114.87 billion in 2026 globally and is expected to hit $273.08 billion by 2031, with APAC delivering the fastest regional growth rate at a 19.92% CAGR. (Mordor Intelligence)

- 96% of APAC enterprises plan to increase AI budgets in 2026, averaging a 15% investment uplift, with infrastructure, data governance, and production-scale deployment as the primary spending targets. (IDC/Lenovo)

These figures do not represent speculative forecast value — they reflect capital already committed, enterprise contracts already signed, and organizational strategies already being restructured around AI. The APAC AI market is not approaching a breakout moment; for many of its leading enterprises, it has already arrived.

The AI Shopping Revolution: 81% of APAC Consumers Demand AI-Powered Tools. More here!

Generative AI and LLMs: The Architecture of New Revenue Streams

Generative AI and Large Language Models are the primary technical layer driving the revenue transformation of 2026. Unlike rule-based automation or narrow AI systems, LLMs can handle unstructured data — customer conversations, regulatory documents, market intelligence feeds, internal knowledge bases — and transform that raw information into commercial decisions at scale.

The business implications are significant. Enterprises are deploying LLM-powered systems across the following high-value functions:

- Hyper-personalized customer engagement: LLM-driven platforms analyze behavioral data, purchase history, and interaction patterns to generate contextually relevant, individualized offers and communications — at a scale no human team can replicate.

- Intelligent product development: Generative AI is accelerating R&D cycles by synthesizing market signals, patent data, and competitive intelligence to identify unmet customer needs and prototype new solutions faster.

- Revenue operations automation: From AI-assisted pricing engines to dynamic contract generation, LLMs are eliminating the lag between commercial opportunity identification and execution.

- Compliance-accelerated financial services: APAC financial institutions are using Generative AI to parse thousands of pages of regulatory documentation in hours rather than weeks, enabling faster product launches and market entries.

A notable real-world example comes from Standard Chartered, which launched an AI-powered compliance and trading assistant in 2025, delivering regulatory guidance and market intelligence access that significantly reduced decision turnaround times. Meanwhile, Singapore's OCBC Bank reported a 50% efficiency gain following a six-month AI chatbot trial — gains that translated directly into redeployment of human capital toward higher-value revenue activities.

The shift from LLMs as exploratory tools to LLMs as core commercial infrastructure is the defining technical dynamic of the 2026 APAC AI market.

AI Investments Set to Outpace Digital Tech Spending in Asia-Pacific, Driving $1.6 Trillion Economic Impact by 2027. Read here!

AI Chatbots: From Support Function to Customer Revenue Layer

If Generative AI represents the strategic architecture of APAC's AI transformation, then the AI Chatbot is its most commercially immediate expression. Across financial services, retail, healthcare, and telecommunications, conversational AI platforms have moved far beyond FAQ automation — they are now functioning as intelligent revenue interfaces.

In APAC banking specifically, this evolution is accelerating rapidly. The global conversational AI in banking market was valued at $2.13 billion in 2024, growing at a 22.7% CAGR through 2033, with APAC emerging as the primary growth engine. According to the Infosys Bank Tech Index 2025, AI now represents approximately 9% of technology budgets across regional banks — a figure that continues to rise.

By 2026, leading APAC banking platforms are deploying AI chatbot systems capable of:

- End-to-end transactional support — using retrieval-augmented LLMs to handle loan inquiries, account management, and digital onboarding with full contextual awareness.

- Cross-sell and upsell intelligence — delivering personalized product recommendations based on real-time financial behavior rather than static customer segments.

- Multilingual KYC and compliance workflows — automating document verification and identity checks across Southeast Asia's highly multilingual customer base, delivering up to 20% faster onboarding cycles compared to 2024 benchmarks.

- Relationship manager augmentation — AI copilots in Singapore's and Hong Kong's private banking divisions assist advisors with client profiling, compliance checks, and risk analysis in real time.

The economics of this shift are compelling. Research from McKinsey and Juniper Research places the unit cost of an AI-resolved customer interaction at approximately $0.50–$0.70, compared to $6–$8 for a human-handled case — a 10 to 12 times cost advantage that compounds significantly at enterprise conversation volumes.

Beyond banking, APAC's retail, e-commerce, and telecommunications sectors are scaling similar AI Chatbot deployments. LUXGEN, a Taiwanese electric vehicle brand, deployed an AI agent on its official LINE account, reducing human customer service workload by 30% while maintaining response quality. These outcomes illustrate a consistent pattern: AI Chatbots are not replacing the customer relationship — they are expanding the enterprise's capacity to serve, personalize, and convert customers at unprecedented scale.

Deloitte Report : AI Governance Improvement Opportunities in the APAC Region. Read more here!

Industry-by-Industry: Where AI Revenue Growth Is Most Concentrated

The APAC AI Outlook 2026 makes clear that AI revenue impact is not uniform across industries — it is concentrated in sectors where data richness, customer interaction volume, and regulatory complexity create the highest return on AI deployment.

Financial Services and Banking

APAC's banking sector stands as the region's most advanced AI adopter. According to Juniper Research projections cited by Statista, global banking Gen AI spend is forecast to rise from approximately US$6 billion in 2024 to roughly US$85 billion by 2030. McKinsey's Global Institute separately estimates that Generative AI could deliver US$200–$340 billion in annual banking value — equivalent to 9–15% of operating profits — for early-adopting institutions. Regional leaders including DBS, OCBC, and Standard Chartered have moved from isolated AI pilots to organization-wide deployment strategies.

Telecommunications

Telecom operators across APAC face intense margin pressure and fierce competition for customer loyalty — conditions that make AI adoption commercially urgent rather than merely strategic. NVIDIA's State of AI 2026 report identifies telecommunications as the industry with the highest rate of agentic AI adoption at 48%, as carriers deploy AI to personalize plans, automate network operations, and reduce churn through predictive intervention.

Healthcare and Life Sciences

Healthcare AI in APAC is being driven by the region's demographic pressures — aging populations in Japan and South Korea, and rapidly growing middle-class healthcare demand across Southeast Asia and India. The enterprise AI market for healthcare is projected to grow at a 20.77% CAGR through 2031, with clinical decision support, patient engagement AI, and AI-assisted diagnostics leading deployment.

Manufacturing and Supply Chain

China, South Korea, Taiwan, and Japan remain APAC's manufacturing powerhouses, and AI is fundamentally restructuring their competitive models. Predictive maintenance, AI-driven demand forecasting, and quality inspection automation are reducing operational losses while AI-powered supply chain optimization is unlocking working capital efficiencies previously inaccessible at scale.

Retail and E-Commerce

Customer-facing AI functions led enterprise deployment in 2025 with 38.91% of total Enterprise AI market spending, and this trend is intensifying in 2026 as personalization engines, dynamic pricing AI, and conversational commerce platforms become table-stakes competitive requirements across APAC's high-growth retail markets.

AI Investment a Top Priority for Asia-Pacific Entrepreneurs, UBS Report Finds. Continue reading here!

Enterprise AI Adoption: Where APAC Stands — and Where It Must Accelerate

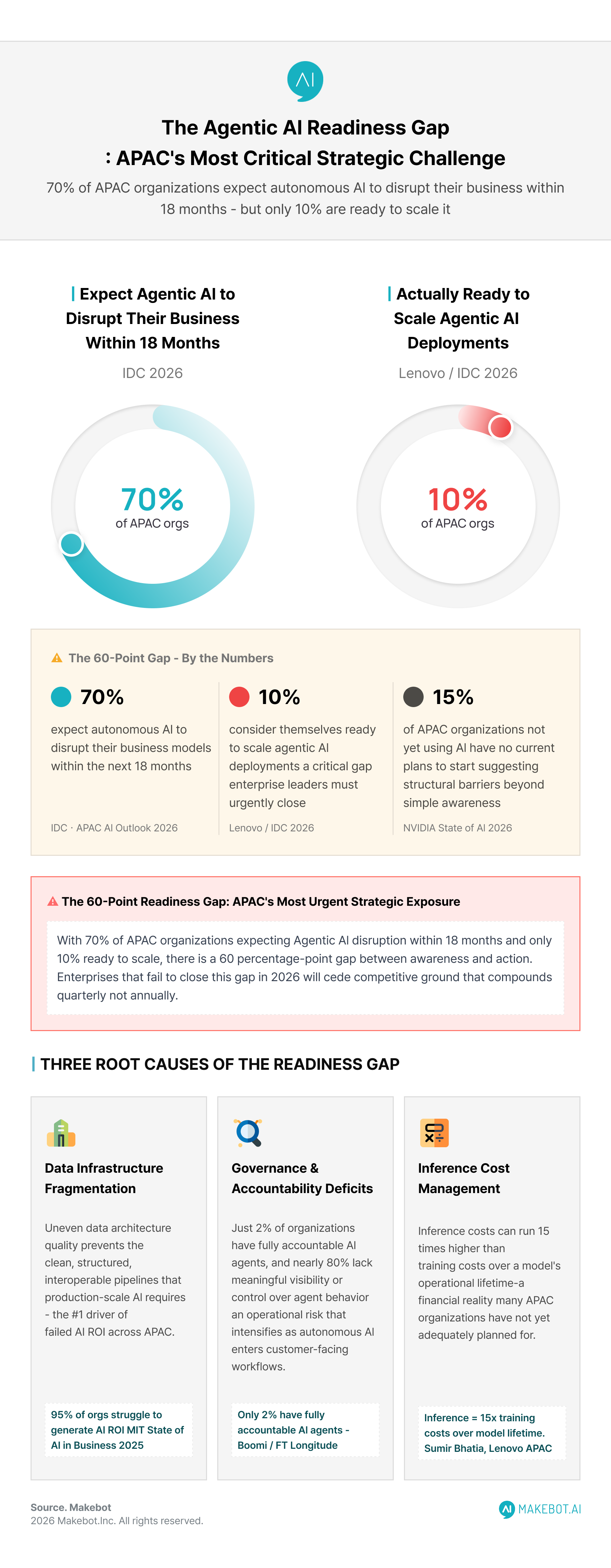

Enterprise AI adoption in APAC is running at a high pace but revealing a critical maturity gap. According to NVIDIA's 2026 State of AI report, 63% of APAC organizations are actively using AI — slightly behind North America's 70% but aligned with European adoption rates. Of those not yet deploying AI, 15% have no current plans to start, a number that suggests structural barriers beyond simple awareness.

The more critical constraint is readiness for the next generation of AI capability. While 60% of APAC organizations are exploring or planning limited deployments of agentic AI, only 10% consider themselves ready to scale such systems. This gap — between interest and readiness — defines the central strategic challenge for APAC enterprises in 2026.

Three barriers consistently emerge across the region:

- Data infrastructure fragmentation: Uneven data architecture quality means many organizations cannot provide the clean, structured, interoperable data pipelines that production-scale AI requires. MIT's State of AI in Business 2025 found that 95% of organizations struggle to generate meaningful ROI from AI, largely attributable to weak data foundations.

- Governance and accountability deficits: Boomi and FT Longitude research reveals that just 2% of organizations have fully accountable AI agents, and nearly 80% lack meaningful visibility or control over agent behavior — an operational risk that becomes acute as autonomous AI systems are integrated into customer-facing workflows.

- Inference cost management: Sumir Bhatia, President of APAC at Lenovo's Infrastructure Solutions Group, has noted that inference costs can run 15 times higher than training costs over a model's operational lifetime — a financial reality many APAC organizations have not yet adequately planned for.

These barriers are surmountable, but they require disciplined investment in data governance, integration architecture, and AI risk management — not just in model deployment.

AI Meets Healthcare: How Asia-Pacific is Pioneering the Next Era of Medtech Innovation. Read here!

The Five Foundational Transformations Shaping APAC AI Leadership

The IBM APAC AI Outlook 2026 identifies five structural transformations that will define enterprise AI leadership across the region through the end of the decade. For business and technology leaders, these represent the strategic architecture within which AI investment decisions must be made.

1. The Internet of AI Generative and agentic AI are evolving into core digital infrastructure — comparable in foundational importance to cloud computing or the internet itself. APAC enterprises are transitioning from centralized data center architectures to distributed, privacy-first ecosystems where AI models operate across smartphones, IoT devices, and edge compute nodes. On-device inference and persistent memory design are unlocking broader adoption while lowering the cost and complexity of scale.

2. AI as a Growth Multiplier Efficiency gains are table stakes. The most strategically advanced organizations are deploying AI to reinvent business models, create new product categories, and unlock differentiated market positions. AI, in this formulation, is not a cost management tool — it is a compounding growth asset.

3. Transferable Value Across Industries The APAC market is beginning to realize the value of AI capabilities that cross sector boundaries — compliance intelligence developed in financial services being repurposed for healthcare; personalization engines built for retail being adapted for telecom customer retention. Cross-industry AI transferability accelerates competitive advantage for organizations that treat AI as a portfolio asset rather than a department-specific tool.

4. Governance as a Competitive Advantage Singapore's Monetary Authority has set the regional benchmark for responsible AI governance, emphasizing fairness, explainability, and auditable decision-making. Increasingly, governance is not just a compliance requirement — it is a trust asset that differentiates enterprises in regulated markets and in customer-facing AI applications where trust determines adoption.

5. AI-Native Business Architecture The most advanced APAC organizations are not retrofitting AI onto existing business processes — they are redesigning organizational structures, talent models, and technology stacks around AI-native workflows. This architectural shift represents the deepest form of competitive differentiation and the hardest for laggards to reverse-engineer.

Strategic Implications for Enterprise Leaders

The APAC AI Outlook 2026 is not simply a market intelligence document — it is a strategic mandate. For enterprise leaders navigating this landscape, several implications are clear:

Move from pilot to production with discipline. The window for treating AI as experimental is closing. Organizations that remain in pilot mode while competitors scale production deployments will accumulate a structural disadvantage that compounds quarterly, not annually.

Align AI investment with revenue architecture. AI spending that cannot be traced to a customer experience improvement, a new revenue stream, a product acceleration, or a measurable market share gain should be restructured. The era of AI as R&D indulgence is over; every deployment should carry a commercial thesis.

Build governance before you need it. The enterprises that will dominate APAC's AI landscape through 2030 are those investing in governance infrastructure today — before regulatory mandates force reactive compliance spending. Data lineage, model explainability, and audit trail capabilities are competitive assets, not overhead.

Prioritize agentic AI readiness. With IDC projecting that 70% of APAC organizations expect agentic AI to disrupt their business models within 18 months, enterprises that begin building the data architecture, integration layers, and human oversight frameworks for autonomous AI systems now will have a decisive head start.

.jpg)

.png)

_2.png)