7 Proven Factors That Drive AI ROI in 2026, According to a Survey of 1,000+ Executives

Only 5.5% of enterprises see real AI ROI — 7 organizational factors that separate leaders from rest.

Introduction

The AI investment story of the mid-2020s is one of growing commitment and uneven returns. Enterprises around the world are doubling down on their AI investment strategy: according to Deloitte's 2025 survey of 1,854 senior executives, 85% of organizations increased their AI investment in the past twelve months, and 91% plan to increase it again. Yet despite this momentum, the share of companies capturing meaningful return on AI investments remains surprisingly small.

The question is no longer whether AI can generate value—most executives believe it can. The harder and more urgent question is: what actually determines whether it does?

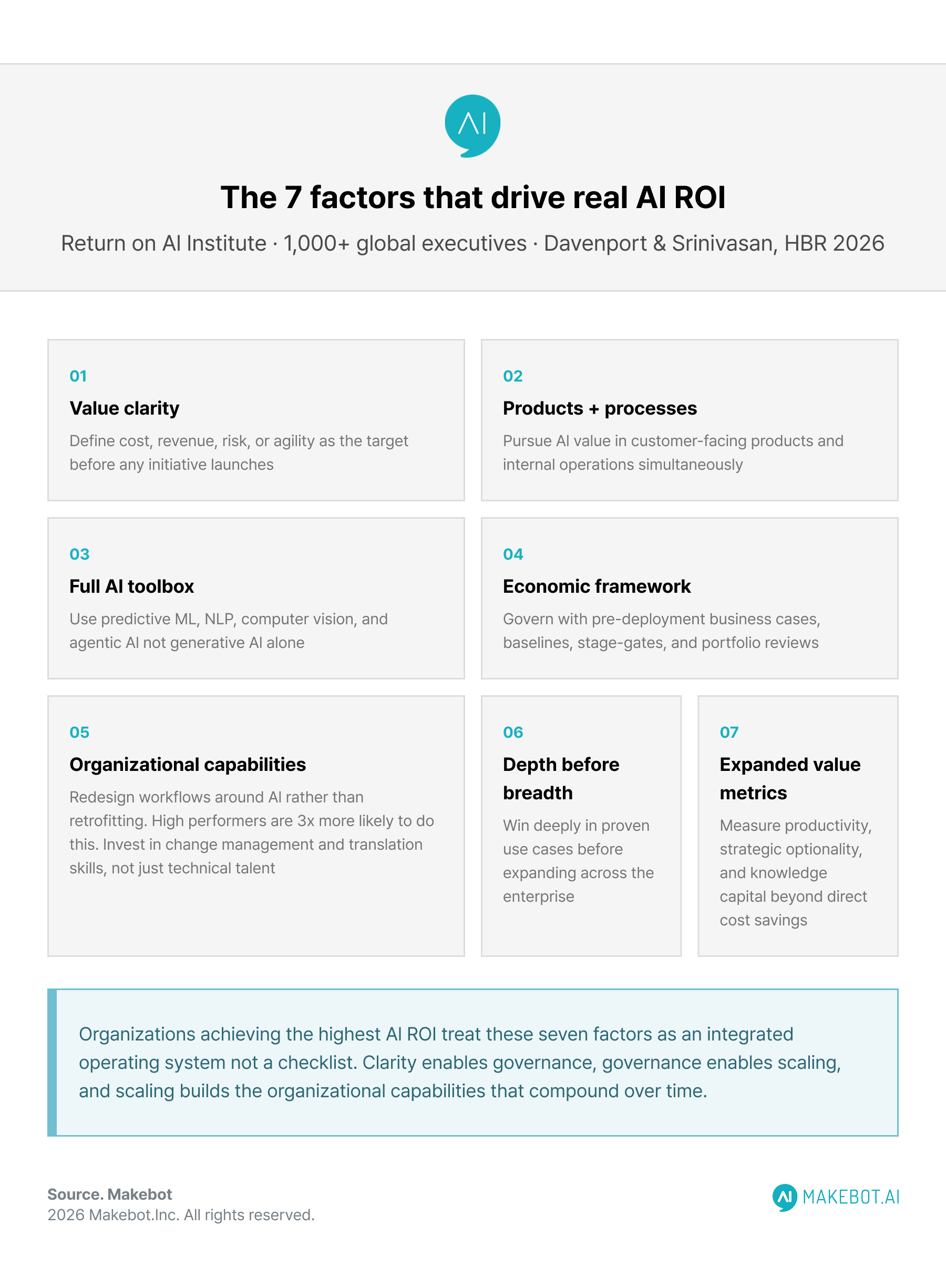

A new survey by Thomas H. Davenport of Babson College and MIT, and Laks Srinivasan, CEO of the Return on AI Institute, offers some of the clearest answers yet. Drawing on responses from more than 1,000 global executives and in-depth interviews with twelve AI leaders, their research identifies seven specific factors that reliably drive economic value from AI—and several of them run counter to conventional wisdom.

Deloitte Insights: AI Fluency Becomes the Most Valuable Workforce Skill. Read more here!

The AI ROI Paradox: High Investment, Uneven Returns

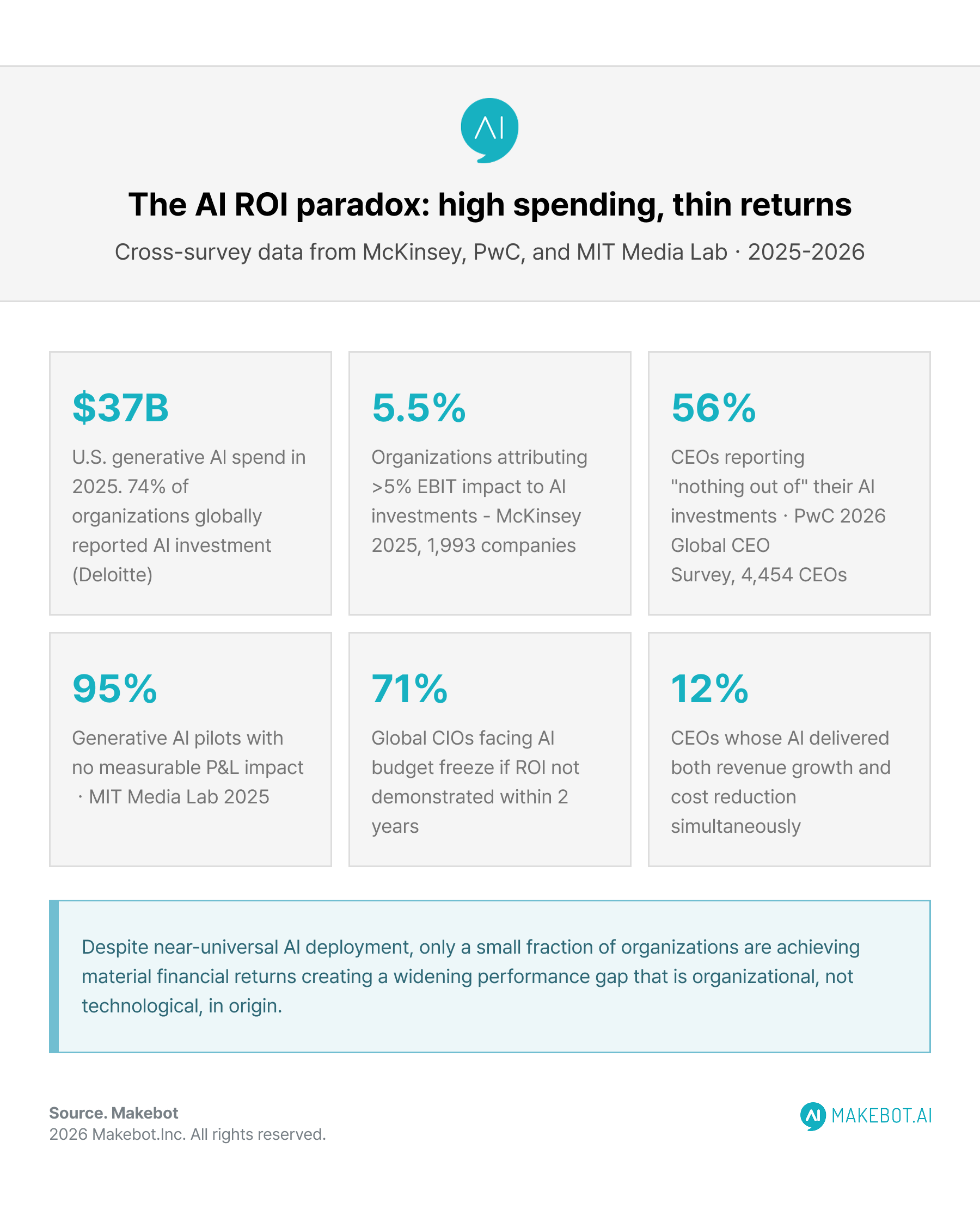

Before examining the seven factors, it's worth understanding just how wide the performance gap has become. McKinsey's 2025 State of AI report, based on responses from 1,993 companies, found that only about 5.5% of organizations are attributing more than 5% of EBIT impact to their AI investments. Meanwhile, MIT Media Lab's "The GenAI Divide: State of AI in Business 2025" report—drawing on 300 public AI deployments, 52 executive interviews, and surveys of 153 leaders—found that despite $30–40 billion in enterprise generative AI spending, 95% of generative AI pilots are delivering no measurable P&L impact.

The contrast is stark against the investment backdrop. Generative AI ROI has become the defining pressure point for enterprise leaders: U.S. companies spent $37 billion on generative AI alone in 2025, yet the majority have little to show for it financially. Deloitte's separate 2025 tech value survey found that AI and generative AI were the clear front-runners across 20 technology capability categories, with 74% of surveyed organizations reporting investments—nearly 20 percentage points ahead of the next most-invested area. These AI adoption trends signal near-universal deployment, but not near-universal returns.

PwC's 2026 Global CEO Survey of 4,454 CEOs across 95 countries adds another layer of concern: 56% reported getting "nothing out of" their AI investments, and only 12% said AI had both grown revenues and reduced costs simultaneously.

This is the paradox that the Return on AI Institute survey was designed to unpack. What separates the organizations seeing genuine AI business value from the vast majority still searching for it?

Deloitte: 70% of Leaders Prioritize Agility as AI Reshapes Business Strategy. More here!

Factor 1: Clarity on the Type of Value Being Pursued

The first and arguably most foundational factor is organizational clarity—specifically, being explicit about what kind of economic value the organization is trying to achieve before any AI initiative is launched.

The survey found that organizations with well-defined, outcome-anchored AI investment strategy significantly outperformed peers who adopted AI under more general mandates like "improve efficiency" or "stay competitive." This aligns with findings from McKinsey's research, which identified tracking well-defined KPIs as the single most important organizational practice for AI success—and noted that high performers establish measurement frameworks before deployment, not after.

The distinction matters because "AI value" is not monolithic. Organizations can pursue:

- Cost reduction through automation and process efficiency

- Revenue growth through new product capabilities or customer experiences

- Risk mitigation through fraud detection, compliance monitoring, or predictive maintenance

- Strategic agility through faster decision-making and competitive intelligence

Each type of value demands different use cases, different metrics, and different timelines. Enterprises that conflate them tend to underperform on all of them. Clarity is not a soft capability—it is the foundation everything else is built on.

LLM Optimization for B2B Marketing: Architecture, RAG Pipelines, and AI Strategies for Enterprise Growth. Continue reading here!

Factor 2: Seeking Value in Both Products and Processes

One of the more counterintuitive findings from the survey is that organizations pursuing AI value exclusively in internal processes—operations, cost centers, back-office automation—tend to generate significantly lower returns than those simultaneously embedding AI into customer-facing products and services.

Deloitte's AI ROI Leader analysis supports this: the top 20% of AI performers were significantly more likely to define their most critical AI wins in strategic terms, with 50% citing "creation of revenue growth opportunities" and 43% citing "business model reimagination" as their primary value drivers—not operational savings.

The practical implication is that enterprise AI adoption strategies need to be dual-track. Process efficiency gains are real and measurable, but they tend to be finite, one-time improvements. Product and service innovation, on the other hand, creates compounding advantages—new revenue streams, improved customer loyalty, and differentiation that competitors cannot easily replicate.

McKinsey's data reinforces this: AI high performers are more likely than peers to report active AI use in marketing and sales, strategy and corporate finance, and product and service development—not just in IT and operations.

Why McKinsey Says AI Won’t Take Your Job. Click here to read more!

Factor 3: Using All the Tools in the AI Toolbox

Many organizations have equated "AI strategy" with "generative AI strategy"—an understandable mistake given the extraordinary attention generative AI has received since 2023. But the Return on AI Institute survey found that enterprises generating the highest returns are deliberately using a broader set of AI capabilities: predictive analytics, machine learning classifiers, computer vision, NLP, optimization models, and agentic AI systems—alongside generative AI.

This matters because different business problems require different approaches. Fraud detection is better served by supervised machine learning than by a large language model. Demand forecasting responds well to time-series models. Customer service augmentation may benefit from a combination of conversational AI and retrieval-augmented generation. Organizations that treat generative AI as a universal solution leave substantial generative AI ROI on the table—while competitors leveraging the full spectrum of tools pull ahead.

Current AI adoption trends confirm this gap is widening. McKinsey's 2025 State of AI report noted that agentic AI—systems capable of planning and executing multi-step workflows—is rapidly emerging as the next frontier, with 23% of respondents already scaling agentic systems and 39% experimenting. AI implementation success at the enterprise level increasingly depends on how intelligently organizations mix and match these capabilities, not just how broadly they deploy them.

Why Most Enterprise Chatbot Projects Fail Before They Begin. Learn more here!

Factor 4: Adopting a Structured AI Economic Framework

The fourth factor is arguably where the sharpest divide between high performers and laggards appears. Organizations that achieve strong AI investment ROI do not improvise their way to value—they govern it deliberately through structured frameworks that connect AI initiatives to financial outcomes.

This includes:

- Pre-deployment business case modeling that ties each use case to a specific revenue, cost, or risk metric

- Baseline measurement established before AI is deployed (organizations that skip this step cannot prove ROI after the fact)

- Stage-gate reviews that scale funding based on realized metrics, not enthusiasm or progress milestones

- Portfolio governance that regularly reallocates resources away from underperforming initiatives

Deloitte's survey found that 25% of organizations cite inadequate infrastructure and data as a barrier to AI investment ROI—but the more pervasive barrier is the absence of governance frameworks that make accountability operational rather than theoretical. Organizations that frame AI as a technology experiment rather than a value program consistently fail to achieve enterprise-scale AI business value.

From Pilot to Production: How Enterprises Can Successfully Scale LLM Chatbots Across the Organization. Read more here!

Factor 5: Building the Right Organizational Capabilities

Technical capability alone does not explain why some organizations generate dramatically better return on AI investments than others. The Return on AI Institute survey confirmed what McKinsey has described as the core insight of its 2025 State of AI research: AI high performers are distinguished by organizational practices, not technology choices.

Specifically, high performers are nearly three times as likely as their peers to have fundamentally redesigned workflows around AI capabilities rather than layering AI onto existing processes. McKinsey's relative weights analysis of 31 organizational variables found that workflow redesign has one of the strongest contributions to achieving EBIT impact of all factors tested.

The organizational capability dimension also encompasses talent. Skilled AI practitioners remain in short supply globally. But the survey findings suggest that the more critical scarcity is not technical talent—it is the capacity to translate AI outputs into operational decisions, and to lead the change management required when workflows are fundamentally restructured.

Deloitte's research indicates that most organizations need at least 12 months to work through enterprise AI adoption challenges—including workforce training, governance, and integration—before realizing major value from generative AI. Enterprises that underinvest in people development alongside technology deployment consistently fall behind this curve.

Redefining talent in the AI era: From Tool Proficiency to Enterprise Advantage. More here!

Factor 6: Pursuing Depth Before Breadth in Use Case Selection

A recurring pattern among organizations struggling with AI implementation success is the temptation to deploy AI broadly and simultaneously—across functions, geographies, and business units—in order to demonstrate enterprise-wide commitment. The survey data suggests this approach is counterproductive.

Organizations that achieve the strongest return on AI investments focus intensively on a small number of high-impact use cases in proven areas before expanding. Deloitte's research explicitly notes that spreading AI initiatives across too many areas simultaneously produces meaningful results in none of them.

The functions with the most consistently documented early-stage ROI include:

- Customer operations and care, where generative AI can deliver 30–45% productivity improvement according to multiple independent studies

- Marketing and sales, where personalization, lead scoring, and content generation have well-established ROI pathways

- IT and software development, where AI-assisted coding and service desk automation are delivering measurable efficiency gains

- Fraud detection and risk management, where predictive models have a long track record

Scaling from proven use cases creates organizational learning, establishes credibility with finance teams, and generates the operational data needed to refine subsequent deployments. Enterprises that chase breadth before depth rarely build the institutional expertise required for sustained AI transformation.

Stanford AI Experts’ Predictions in 2026. Continue reading here!

Factor 7: Measuring Value Beyond Traditional Financial Metrics

The final factor is perhaps the most strategically important for long-term AI business value realization. The Return on AI Institute survey, along with Deloitte's parallel research, found that organizations achieving the highest AI returns have expanded their definition of value beyond immediate financial metrics.

This is not a license to avoid accountability—quite the opposite. It reflects the structural reality that AI creates value along multiple dimensions simultaneously:

- Productivity and throughput gains that don't immediately translate to revenue but reduce cost-per-outcome

- Strategic optionality, meaning the capacity to enter new markets, launch new products, or respond to competitive threats faster than rivals

- Organizational learning and knowledge capital, built by running AI at scale — McKinsey's State of AI research finds that high performers are significantly more likely to use AI across multiple business functions simultaneously, compounding their institutional advantages over time

- Data infrastructure maturity, where each AI deployment improves the underlying data systems that future deployments rely on

Deloitte's 2025 survey found that 65% of respondents now consider AI as part of corporate strategy—recognizing that not all returns are immediate or financial. This signals a meaningful shift: enterprises are beginning to account for AI's long-term transformation value, not just its short-cycle efficiency gains.

Critically, expanding the measurement framework does not mean avoiding accountability. It means building dashboards that track business outcomes and model quality together—and ensuring that every dollar of AI spending connects to a named outcome, whether financial, operational, or strategic.

How AI Chatbots Are Increasing E-Commerce Conversion Rates. Read here!

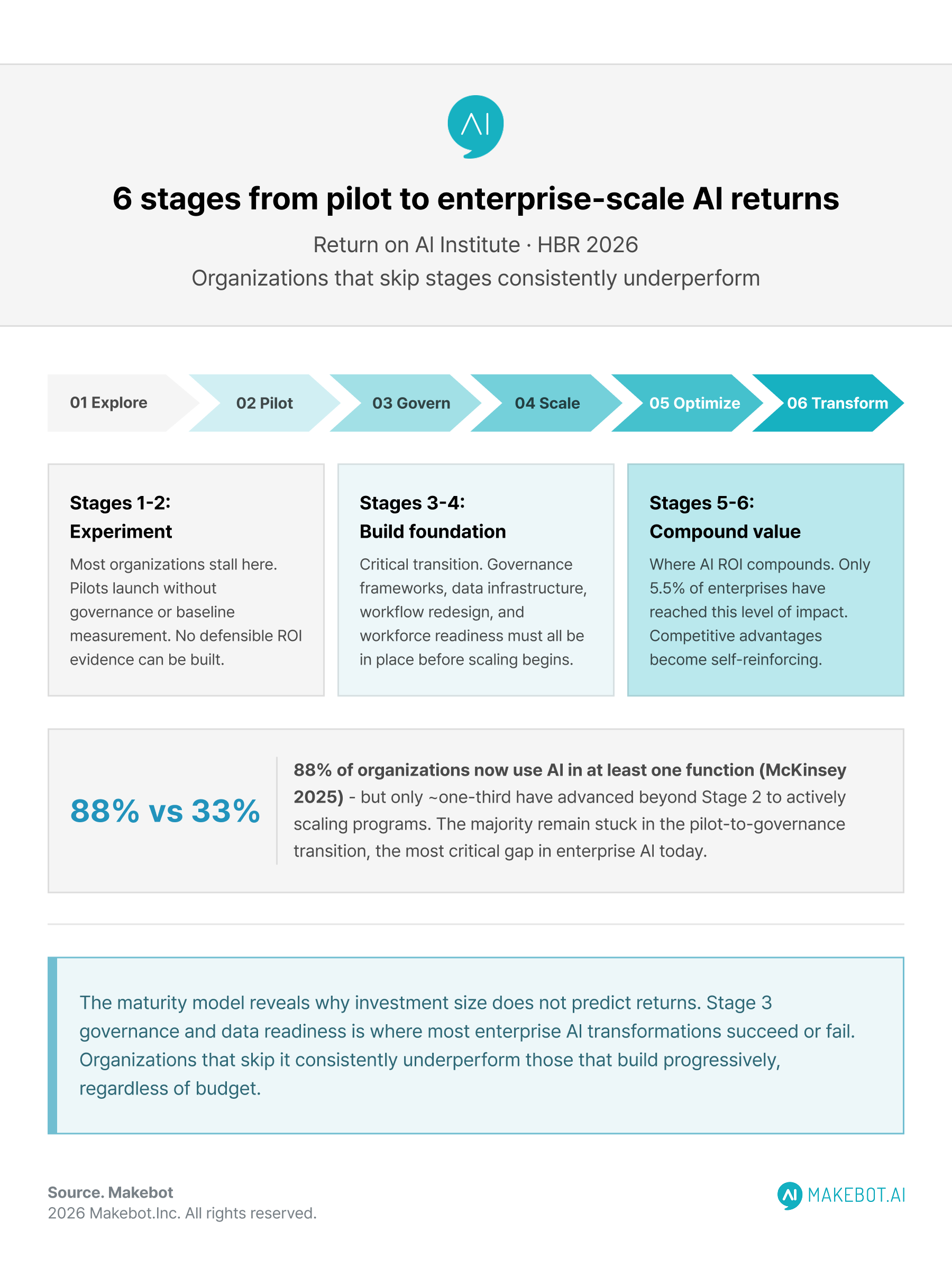

The AI Economic Maturity Model: A Roadmap for Progression

Alongside the seven factors, Davenport and Srinivasan developed a six-stage AI Economic Maturity Model—a research-backed roadmap that maps how organizations typically progress from early pilots to high-value, enterprise-wide returns.

The model reflects a consistent pattern observed across high-performing enterprises: value realization is not a linear function of investment size. It is a function of organizational progression through distinct stages of capability, governance, and strategic integration. Organizations that skip stages—jumping from pilots to enterprise deployment without building governance, data infrastructure, or workforce readiness—consistently underperform.

The model also explains why the performance gap between AI leaders and laggards is widening rather than narrowing, even as adoption becomes nearly universal. Current AI adoption trends show that 88% of organizations now report regular AI use in at least one business function, according to McKinsey's 2025 State of AI. But only approximately one-third have begun scaling their AI programs. The majority remain in the experimenting or piloting stages—facing the exact transition that the maturity model is designed to navigate. For these organizations, the path from enterprise AI adoption to enterprise AI returns runs directly through the maturity model's middle stages: governance, data readiness, and workflow redesign.

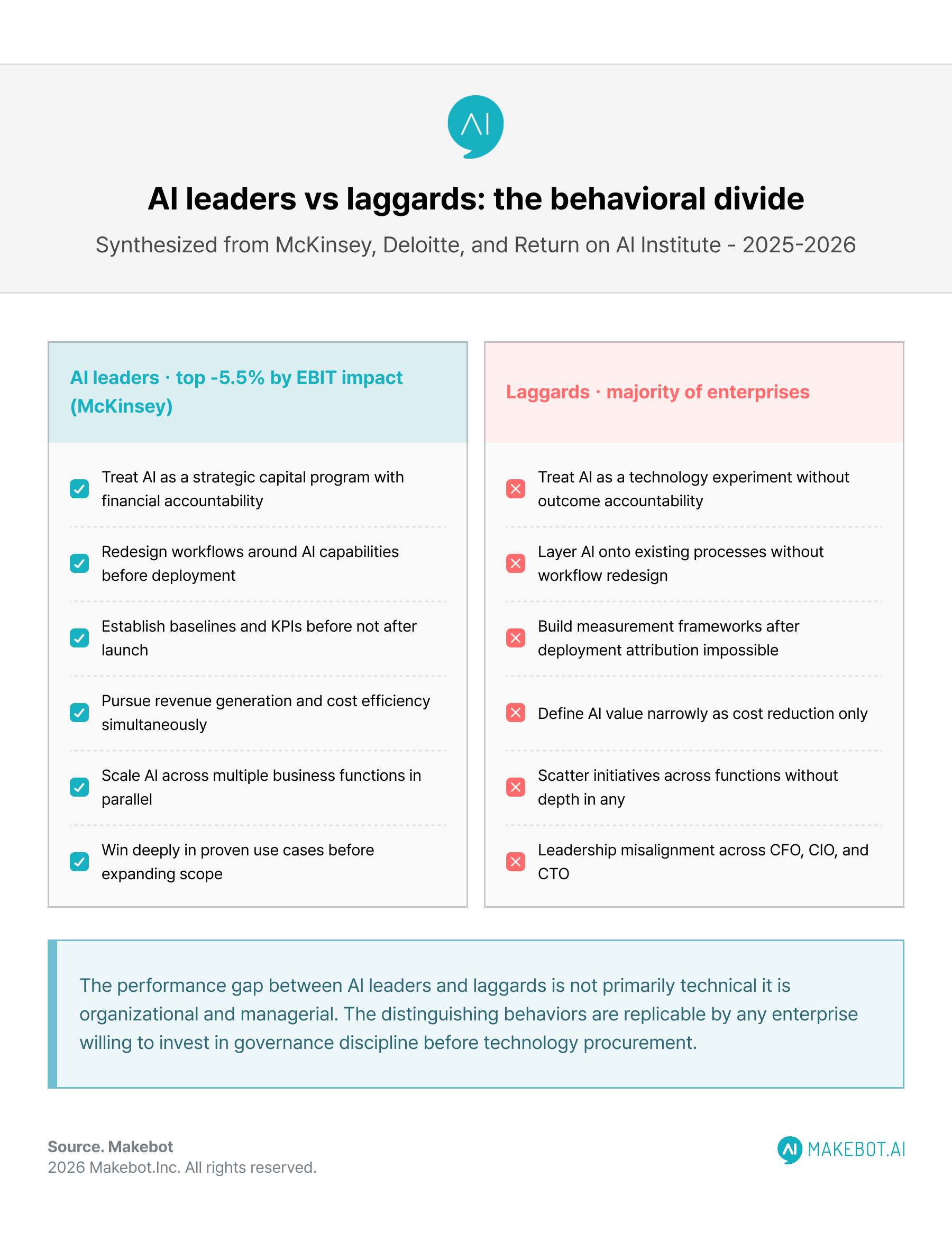

What Separates AI Leaders from the Rest

The aggregate picture that emerges from the Return on AI Institute survey, McKinsey's State of AI research, and Deloitte's 2025 findings is consistent and instructive.

Organizations generating strong AI ROI share several characteristics:

- They treat AI as a strategic program with financial accountability, not a technology experiment

- They redesign workflows around AI capabilities rather than retrofitting AI onto existing processes

- They measure outcomes before and after deployment, creating defensible AI investment ROI evidence

- They invest proportionally in people, governance, and data infrastructure alongside model deployment

- They move fast on proven use cases, then use those wins to fund deeper capability building

Organizations struggling with AI ROI tend to share a different profile:

- AI adoption trends stall at pilot stage — initiatives scattered across many functions without depth in any

- Measurement frameworks built after deployment, making attribution impossible

- Leadership alignment gaps—CFOs, CIOs, and CTOs pulling in different directions

- Workforce readiness underestimated, with enterprise AI adoption challenges taking longer than expected

- AI business value defined narrowly as cost reduction, leaving revenue and strategic gains unrealized

The divide is not primarily technical. It is organizational, strategic, and managerial.

Showcasing Korea’s AI Innovation: Makebot’s HybridRAG Framework Presented at SIGIR 2025 in Italy. Read here!

Conclusion: AI ROI Is Engineered, Not Discovered

The findings from the Return on AI Institute survey—and the broader body of research it synthesizes—arrive at a clear conclusion: the enterprises that will capture disproportionate value from AI over the next decade are not necessarily those with the largest budgets, the most advanced models, or the most enthusiastic boards. They are the ones that approach AI investment strategy with the same discipline they apply to any other major capital program.

With 71% of global CIOs facing budget freezes if they cannot demonstrate AI investment ROI within two years, the window for the industry's current tolerance of undefined returns is narrowing. Generative AI ROI and broader AI business value will increasingly be expected to appear on earnings calls and board presentations—not as aspirational frameworks, but as documented outcomes.

The seven factors identified in this research provide a practical, evidence-based starting point. Clarity of purpose, dual-track value creation, full-spectrum tool deployment, structured governance, organizational capability building, focused use case selection, and expanded value measurement—none of these is technically complex. But together, they constitute the operating system for AI transformation that actually delivers.

The AI era is not a technology race. It is a management challenge. The organizations that internalize that distinction soonest will be the ones writing the return on AI investments case studies that everyone else is trying to replicate.

.jpg)

.png)

_2.png)